Module 7 · Lesson 2

Protecting Your Funded Account

Build a professional protection system using personal loss limits, drawdown buffers, risk zones, reduced-risk rules, and clear conditions that tell you when to stop trading.The prop firm defines the maximum amount you are allowed to lose. A professional trader defines a smaller amount they are willing to lose.

A Funded Account Must Be Defended

Receiving a funded account gives you access to trading capital, but it also places you inside a strict risk environment where one emotional decision can end the opportunity.

Most prop firms provide official limits for daily drawdown, maximum drawdown, trading consistency, prohibited activity, and account inactivity. Those limits tell you when the firm will close the account. They do not tell you how close a professional trader should operate to those boundaries. A trader who repeatedly trades near the firm’s maximum permitted loss is not managing risk professionally. They are using the firm’s emergency boundary as a normal operating limit. The correct approach is to build a second layer of protection inside the official rules. This personal protection system should stop trading before the account reaches serious danger.The firm’s drawdown limit is an account-failure boundary. It should never become your daily risk target.

This lesson builds on The Funded Trader Mindset, Understanding Daily Drawdown, and Maximum Drawdown Explained.

What You Will Learn

1Separate firm limits from personal limits

Understand why your personal boundaries should be tighter than the prop firm’s official rules.

2Calculate available risk capital

Measure the real distance between your current equity and the account’s failure boundary.

3Create protection zones

Use green, caution, reduced-risk, and stop-trading zones to control account exposure.

4Set daily and weekly limits

Prevent one poor session or emotional week from threatening the entire account.

5Know when to reduce risk

Identify account, market, and behavioral conditions that require smaller exposure.

6Know when to stop

Create non-negotiable rules that pause trading before damage becomes irreversible.

Maximum Allowed Risk Is Not Recommended Risk

A prop firm may allow a 5% daily drawdown and a 10% maximum drawdown. That does not mean a trader should willingly lose 5% in one day or operate until only a small amount remains before the maximum limit. Official drawdown limits exist to define failure. Personal risk limits should define professional behavior.Firm LimitThe maximum loss permitted before the account is breached.

Personal LimitThe smaller boundary at which the trader stops or reduces exposure.

Safety BufferThe unused space kept between personal limits and firm failure rules.

- Slippage during volatile market conditions.

- Spread widening around economic news.

- Floating losses on multiple open positions.

- Calculation mistakes involving equity-based drawdown.

- Correlated positions moving against the account simultaneously.

- Platform delays, execution errors, or unexpected disconnections.

- Emotional decisions made after consecutive losses.

Dangerous thinking: “I still have drawdown available, so I can keep trading.” Available drawdown does not mean the next trade is justified.

Understand the Account’s Real Operating Room

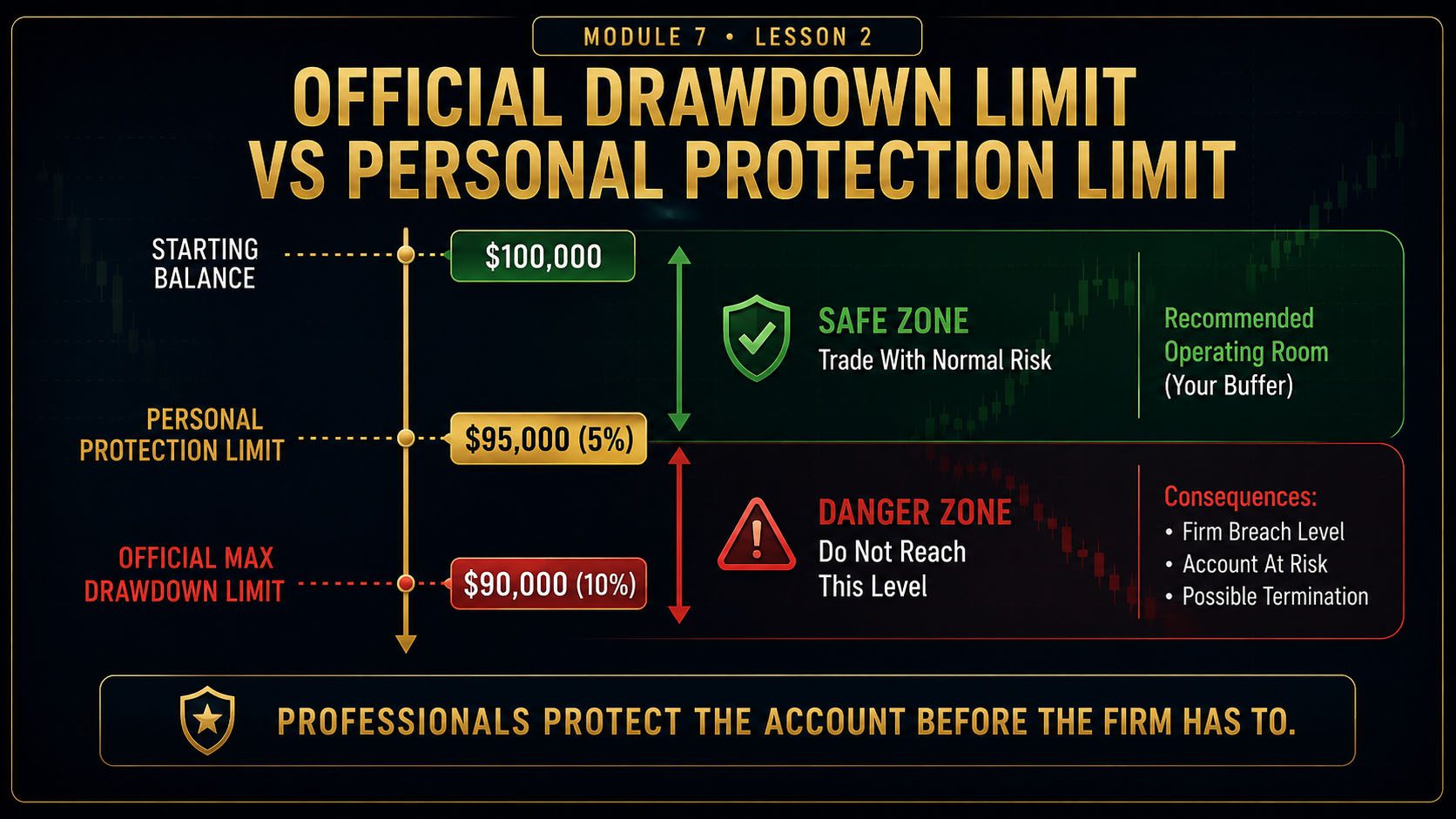

The displayed account balance can be misleading. A $100,000 funded account does not give the trader $100,000 of risk capital. The account may only have a few thousand dollars of permitted drawdown. The amount that matters most is the distance between current equity and the maximum drawdown boundary.Available Risk Capital

Current Account Equity − Account Breach Level

Available Risk Capital = Equity − Drawdown BoundaryExample

Assume a $100,000 funded account has a static maximum drawdown limit of $10,000. The account breach level is therefore $90,000. If the current account equity is $102,500:$102,500 − $90,000 = $12,500

The account currently has $12,500 between its equity and the breach boundary.

That does not mean the trader should risk $12,500. It means this is the account’s total structural room before failure. A professional trader should only use a small controlled percentage of that room.

If the account uses a trailing drawdown rather than a static limit, the boundary may move as the account reaches new highs. Review Static vs Trailing Drawdown before creating your protection plan.

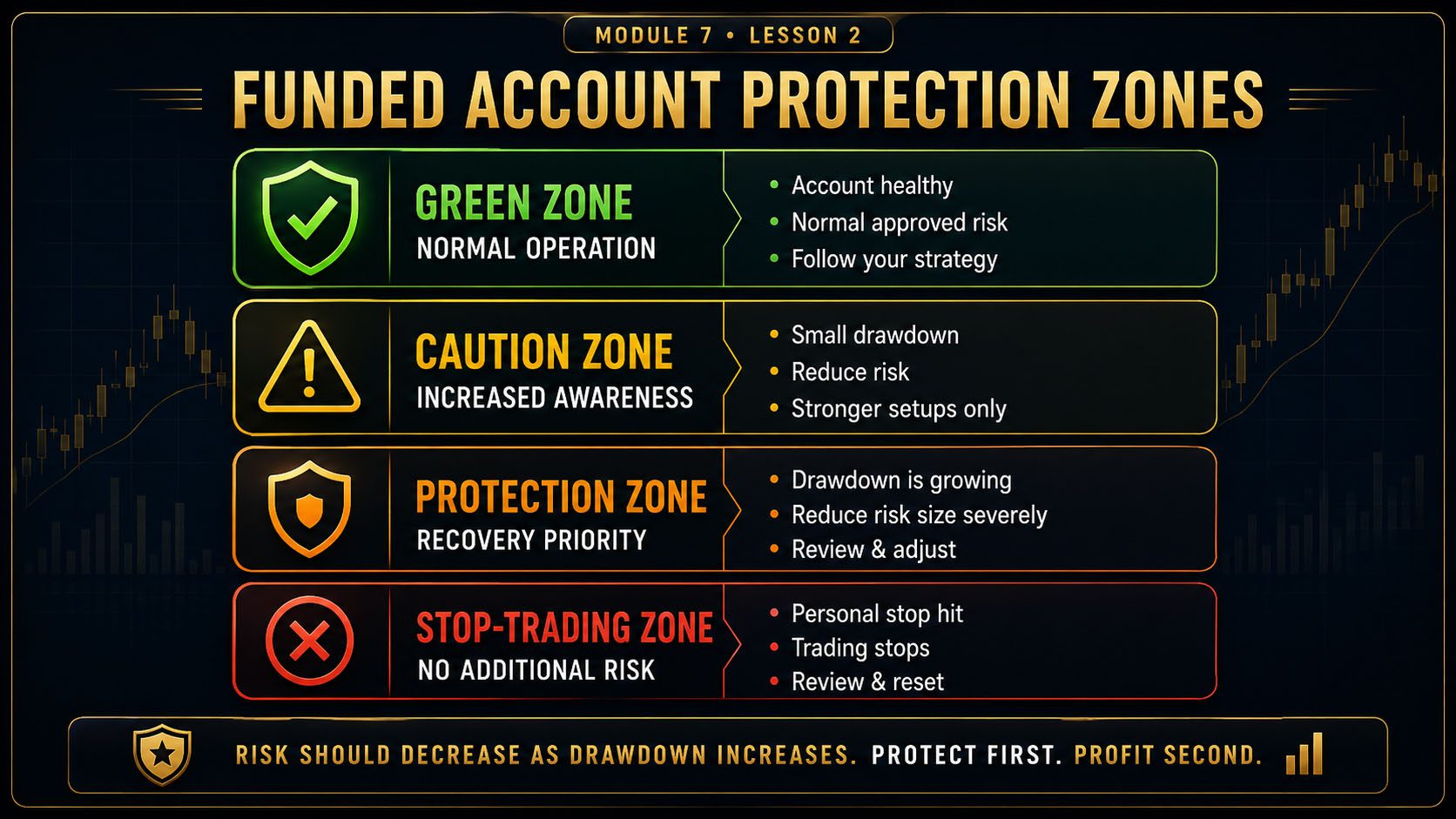

Create Funded Account Safety Zones

A professional protection system should not treat the account as either safe or breached. There should be several operating zones between normal conditions and account failure.Green Zone

Normal controlled operation- Account is near or above its protected starting level.

- Normal approved risk may be used.

- Only tested setups are traded.

- Daily and weekly boundaries remain active.

Caution Zone

Risk awareness increases- Account has entered a modest drawdown.

- Trade frequency is reduced.

- Only the strongest setups qualify.

- Risk may be reduced by 25% to 50%.

Protection Zone

Account recovery becomes the priority- Drawdown is becoming significant.

- Normal risk is no longer permitted.

- Trading may pause for review.

- Execution errors must be separated from valid losses.

Stop-Trading Zone

No additional risk is permitted- Personal maximum loss limit has been reached.

- Trading stops before the firm boundary.

- A formal review is required.

- Return requires a written recovery plan.

The purpose of safety zones is to change behavior before the account reaches danger. Risk should decrease as drawdown increases, not the other way around.

Set a Personal Daily Loss Limit

The daily loss limit is one of the most important funded-account protections because it prevents one poor session from causing serious account damage. Your personal daily loss limit should normally be significantly smaller than the firm’s official daily drawdown rule.| Account Condition | Example Personal Daily Limit | Professional Response |

|---|---|---|

| Account in green zone | 0.75% to 1.5% | Normal approved risk while the setup remains valid. |

| Small drawdown | 0.5% to 1% | Reduce risk and trade only high-quality opportunities. |

| Protection zone | 0.25% to 0.5% | Very limited exposure or complete pause pending review. |

| Personal maximum drawdown reached | 0% | No trading until the account protection review is completed. |

Stop a Bad Week From Becoming a Bad Month

Daily limits protect individual sessions, but they do not prevent a trader from losing a small amount every day for an entire week. A weekly loss boundary provides a second layer of control.Example Weekly Protection Rules

- Stop trading for the week after reaching a predetermined weekly loss percentage.

- Reduce risk after two consecutive losing days.

- Pause after three consecutive strategy losses and review market conditions.

- Stop immediately if losses were caused by repeated rule violations.

- Do not increase Friday risk to repair Monday through Thursday losses.

- Review session, instrument, setup type, and execution quality before restarting.

Never create a “last chance” trade at the end of the week. The market does not care that you want to finish Friday in profit.

When Should Risk Be Reduced?

Risk should not remain fixed under every condition. A professional trader may lower exposure when account conditions, market conditions, or personal conditions deteriorate.Account Conditions

- The account has entered drawdown.

- Several losses have occurred close together.

- The payout buffer has become smaller.

- The account is near a personal protection boundary.

- Multiple correlated positions are already open.

Market Conditions

- Volatility is unusually high or unstable.

- Price action is choppy and lacks structure.

- High-impact news is approaching.

- Spreads or slippage have increased.

- The strategy is experiencing unfavorable conditions.

Trader Conditions

- Confidence has become emotional.

- The trader feels urgency to recover.

- Focus, sleep, or preparation is poor.

- Rules have recently been broken.

- The trader is reacting to money instead of the setup.

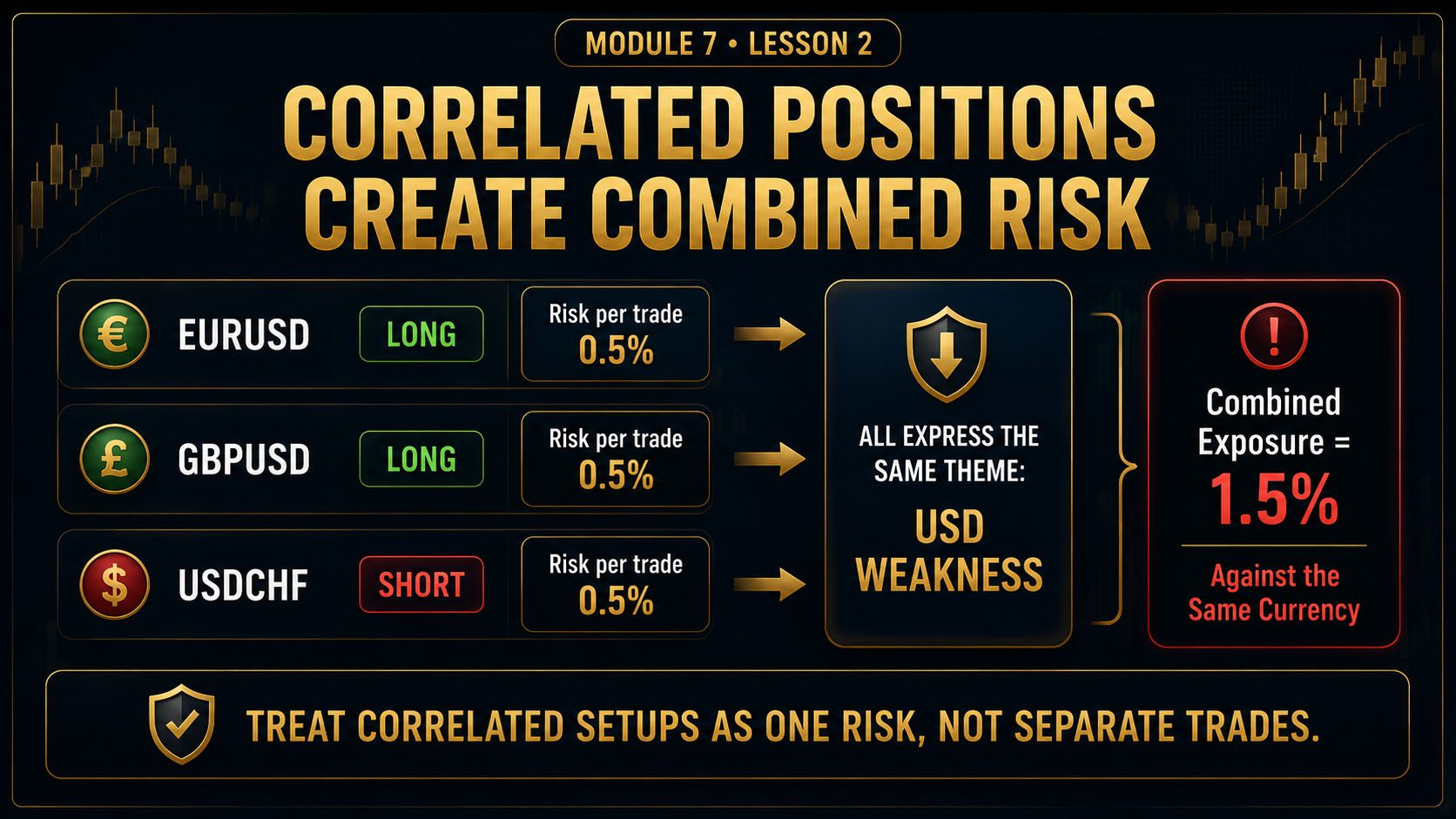

Multiple Trades Can Create One Large Risk

Traders often calculate each trade separately but ignore how several positions may be connected. For example, long EURUSD, long GBPUSD, and short USDCHF may all express a similar view: weakness in the US dollar. If the dollar strengthens unexpectedly, all three positions may lose at the same time.Correlated Risk Example

A trader risks 0.5% on three separate positions:- EURUSD long: 0.5% risk

- GBPUSD long: 0.5% risk

- USDCHF short: 0.5% risk

Conditions That Must Immediately End the Session

A funded-account protection plan must include rules that are automatic and non-negotiable. These conditions should end the session regardless of how strongly the trader wants another opportunity.The personal daily loss limit has been reached.

The firm’s daily drawdown boundary is approaching.

The maximum number of trades has been reached.

Two or more trades were taken outside the strategy.

The trader has moved a stop loss to avoid accepting a loss.

The trader feels compelled to recover money immediately.

Platform, internet, or execution problems create uncertainty.

Unexpected high-impact news disrupts normal conditions.

Open positions create excessive correlated exposure.

The trader is no longer emotionally neutral.

A personal weekly loss boundary has been reached.

The account has entered the stop-trading protection zone.

A stop-trading rule only works when it is followed before the trader feels ready to stop.

Building a Protection Plan for a $100,000 Funded Account

Account Rules

- Starting balance: $100,000

- Official daily drawdown: 5%

- Official maximum drawdown: 10%

- Trader’s normal risk per trade: 0.5%

Personal Protection Rules

- Personal daily stop: 1%

- Maximum two full-risk losses per day

- Personal weekly stop: 2.5%

- Caution zone begins at 2% account drawdown

- Risk reduced from 0.5% to 0.25% in caution zone

- Protection zone begins at 4% account drawdown

- Trading pauses for review in protection zone

- Personal maximum drawdown boundary: 5%

- No trading is permitted below $95,000 equity without a formal recovery plan

Why This Plan Works

The firm allows the trader to lose as much as $10,000 before the account fails. The trader’s personal plan stops normal trading after a $5,000 decline. This leaves a substantial emergency buffer and reduces the probability of an emotional breach.The Professional Funded Account Protection Process

Know Every Firm Rule

Confirm daily drawdown, maximum drawdown, trailing rules, payout conditions, prohibited strategies, and account-reset times.Create Smaller Personal Limits

Set personal daily, weekly, and maximum loss boundaries inside the firm’s official limits.Define Risk Zones

Create normal, caution, protection, and stop-trading zones with specific actions for each level.Control Position Size

Calculate risk before entry and include correlated exposure across all open positions.Reduce Risk Early

Lower exposure when drawdown, volatility, execution quality, or emotional control deteriorates.Stop Before the Account Is in Danger

End the session when a personal boundary is reached instead of continuing toward the firm’s failure limit.Funded Account Protection Checklist

I know the firm’s exact daily drawdown rule.

I know the firm’s exact maximum drawdown rule.

I understand whether drawdown is static or trailing.

I know whether the rule is based on balance or equity.

I have a smaller personal daily loss limit.

I have a personal weekly loss boundary.

I have a personal maximum account loss limit.

I know my current account protection zone.

I reduce risk when the account enters drawdown.

I calculate combined correlated exposure.

I stop after reaching the maximum number of trades.

I stop trading when emotional neutrality is lost.

I do not use the full firm limit as normal risk.

I preserve a buffer for slippage and volatility.

Protecting a Funded Account FAQ

Why should my personal loss limit be smaller than the firm’s limit?

The firm’s limit defines when the account fails. A smaller personal limit creates a safety buffer for slippage, floating losses, correlated exposure, emotional mistakes, and unexpected volatility.How much should I risk per funded trade?

There is no universal number. Many conservative funded traders use a small fraction of one percent, but the correct level depends on strategy expectancy, stop distance, win rate, account rules, and current drawdown. Risk must be low enough to survive a normal losing sequence.Should I use the same risk while in drawdown?

Not automatically. When the account enters a caution or protection zone, reducing risk can slow further damage and create more room for recovery. Risk should never increase because the trader feels pressure to recover.Is it better to stop after a fixed number of losses?

A fixed maximum number of losses can be useful, but it should work together with a financial daily loss limit. Two small losses may be acceptable, while two oversized losses may already exceed the plan.How should I handle correlated trades?

Treat positions driven by the same currency, index, commodity, or market theme as combined exposure. Reduce individual position risk or choose only the strongest setup.What happens if I reach my personal stop but not the firm limit?

Trading should stop. The purpose of the personal boundary is to prevent you from reaching the firm limit. Continuing would make the protection rule meaningless.Can I resume trading later the same day after calming down?

Not if the financial daily stop has been reached. A daily limit is a complete-session boundary, not an emotional timeout. If the issue was technical or psychological and no loss limit was reached, your written plan should determine whether restarting is allowed.What should I do when the account enters the protection zone?

Pause normal trading, review all recent trades, separate valid strategy losses from execution mistakes, evaluate market conditions, and create a written reduced-risk recovery plan before returning.Lesson Quiz

1. What does the prop firm’s maximum drawdown limit represent?

2. Why should a trader create a personal loss limit?

3. What should happen as an account enters deeper drawdown?

4. What is available risk capital?

5. Why are weekly loss limits useful?

6. How should correlated positions be treated?

7. What should a trader do after reaching a personal daily loss limit?

8. What is the purpose of the stop-trading zone?

Quiz Answers

1. B — The maximum drawdown is the point at which the account fails.

2. B — Personal limits create protection before the official breach level.

3. C — Risk should decline as account vulnerability increases.

4. B — Available risk capital is the distance between equity and the breach boundary.

5. B — Weekly boundaries stop repeated daily losses from becoming major drawdown.

6. B — Related trades should be measured as combined exposure.

7. C — The session ends when the personal daily stop is reached.

8. B — The stop zone prevents the account from reaching the firm’s failure limit.

What Professional Account Protection Requires

Firm limits are emergency boundariesThey define failure and should not be used as normal operating risk.

Personal limits create controlDaily, weekly, and total account boundaries should stop trading early.

Drawdown changes behaviorRisk should decrease as the account moves from green to caution and protection zones.

Exposure must be combinedSeveral correlated positions can create one large account-level risk.

Stopping is part of tradingA professional protection system includes conditions that automatically end the session.

Buffers preserve opportunityUnused drawdown protects against volatility, mistakes, and unexpected execution problems.

Protect the Opportunity Before Pursuing the Payout

A funded account must be managed inside two sets of rules: the prop firm’s official limits and the trader’s personal protection limits.

The firm’s rules explain when the account will fail. Your personal rules should stop trading long before that point. This requires daily loss boundaries, weekly limits, drawdown zones, correlated-risk controls, and non-negotiable stop-trading conditions.

A professional trader does not increase risk because an account is in drawdown. Risk is reduced as the account becomes more vulnerable. When personal limits are reached, trading stops even if the firm technically allows more room.

In the next lesson, you will learn how to turn protected account performance into a structured payout strategy without becoming aggressive near withdrawal dates.